k-means clustering

KMeans(n_clusters=k)

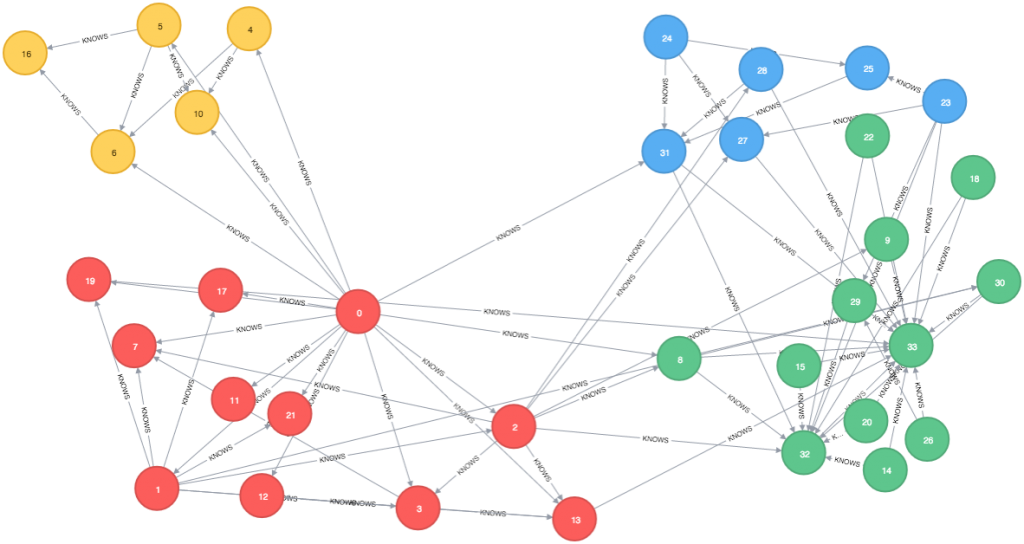

hierarchical clustering

Ward's minimum variance method

by-hand clustering

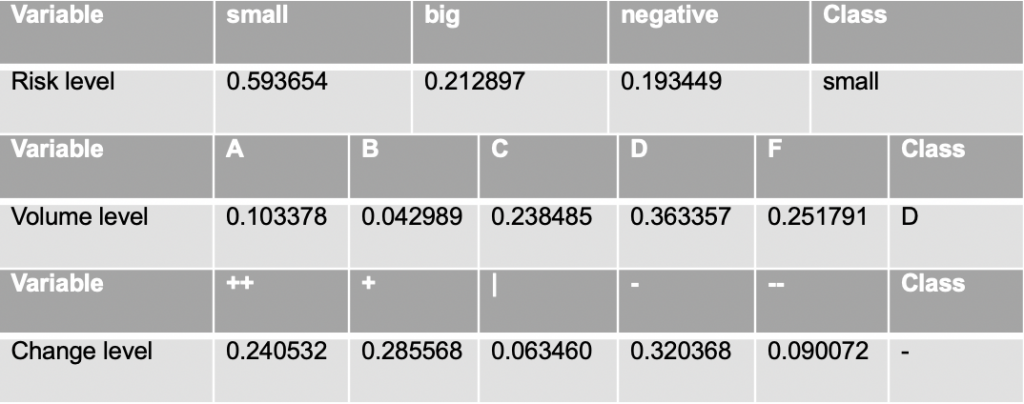

label each sector by proportion

KMeans(n_clusters=k)

Ward's minimum variance method

label each sector by proportion